Specialist Manufacturing's Exit Advantage: Why 2026 is Your Strategic Window to Sell

Beyond the EBITDA Multiple: Capturing Strategic Value in the 2026 Manufacturing Market

If you own a specialist manufacturing business in the UK, your timing may be better than you think. While the broader economic headlines often focus on volatility, the ground-level reality for high-quality industrial SMEs is one of significant opportunity.

The Quiet Boom in Manufacturing M&A

You've spent years - possibly decades - building a specialist manufacturing business. You know the weight of every investment in plant and machinery, every hard-won customer contract, and every Friday afternoon when you wondered whether the stress was worth the reward. The M&A market in early 2026 is providing a clear answer: it was.

After the transitional uncertainty of 2023 and 2024, the UK's mergers and acquisitions landscape has reached a period of productive stability. Inflation has settled into a predictable range, and the Bank of England's previous rate cuts have filtered through to more favourable borrowing conditions. This macro-stability has unlocked a "dam-break" effect, where transactions that were paused in 2025 are now being executed with confidence.

For specialist manufacturers, the momentum is particularly potent. Manufacturing M&A activity rebounded strongly through late 2024 and maintained a high baseline of investment throughout 2025. This positive trajectory is carrying into 2026, supported by three powerful tailwinds: government investment incentives, a structural shift toward supply chain security, and an unprecedented pool of private equity capital seeking defensive, asset-backed UK businesses.

Three Tailwinds Driving Premium Valuations

1. Capital Allowances: Enhancing Buyer Economics

From January 2026, the landscape for capital investment shifted with the application of a new 40% first-year capital allowance for qualifying plant and machinery. If you operate a capital-intensive manufacturing site, this is a critical value driver. It is not merely a benefit for your current tax return; it is a fundamental component of how a buyer models the post-acquisition cash flows of your business.

When a sophisticated buyer - whether trade or private equity - evaluates your company, they are looking at the "net" cost of future growth. Generous capital allowances effectively subsidise the buyer's future investment in your facility, which supports a higher entry multiple. However, this is balanced by the reduction of the annual allowance for tax depreciation to 14% from 2026. This slower rate of writing down assets increases future taxable profits over the long term.

🚩 Diligence Flag: Deferred Maintenance is a Price Chip

Buyers will send a surveyor to your facility. If you've held back on replacing a CNC machine or repairing the roof to "boost" your cash flow before a sale, the buyer will simply deduct the cost of those repairs from the purchase price - often at a 2x penalty for the "hassle factor." It is almost always cheaper to fix the plant yourself than to let a buyer use it as a reason to chip your valuation.

The strategic takeaway is that you cannot leave the tax narrative to the buyer's due diligence team. Work with your specialist tax adviser to model the net effect of these 2026 changes on your business's post-acquisition economics. By presenting a clear, well-reasoned analysis of how the new regime benefits a successor, you transform a dry accounting point into a powerful negotiating lever.

2. The £178 Billion Private Equity "Dry Powder" Pressure

Private equity firms are currently sitting on an estimated £178 billion in undeployed capital. This "dry powder" represents significant pressure for fund managers who must deploy capital to generate returns for their investors. In 2026, the "flight to quality" has led these funds directly to the doorsteps of specialist UK manufacturers.

PE buyers are particularly drawn to businesses that offer what we call "defensible niches." They are looking for predictable revenue streams, proprietary processes, and the potential for "bolt-on" acquisitions where your business serves as a platform to buy smaller competitors. If your business operates in the £1m–£40m turnover range, you are currently in the sweet spot of M&A activity. Transactions valued below £100 million accounted for nearly 90% of all UK M&A volume in the previous year.

International appetite remains a defining feature of the 2026 market. US-based bidders continue to see UK specialist manufacturing as undervalued compared to North American equivalents, often participating in over a third of all firm offers. When you combine domestic PE interest with trade buyers from the US, Middle East, and Asia, you create the competitive tension necessary to drive a valuation beyond standard industry multiples.

3. Reshoring and the Sovereignty Premium

The disruptions of the early 2020s fundamentally rewrote the corporate playbook on supply chains. The trend toward reshoring - bringing critical manufacturing capability back to the UK or near-shoring it to stable allies - is no longer a temporary reaction; it is a permanent strategic pillar.

If your business produces specialist components, works with advanced materials, or serves high-stakes sectors such as defence, aerospace, medical devices, or renewable energy, you possess strategic value that transcends your P&L. Trade buyers are increasingly willing to pay a "sovereignty premium" for guaranteed capacity and security of supply. They aren't just buying your EBITDA; they are buying the certainty that their own production lines won't grind to a halt due to geopolitical instability.

However, this strategic importance brings its own requirements. The National Security and Investment Act (NSIA) remains a vital consideration for manufacturers in sensitive sectors. Advanced materials and specialist manufacturing are explicitly covered. While the NSIA is rarely a deal-killer, it requires mandatory notification and can add weeks to a completion timeline. Identifying whether your business falls under these 17 sensitive sectors is a task for your advisory team long before you sign a Heads of Terms.

The Reality of the 2026 Tax Landscape

As we stand in March 2026, it is important to be pragmatic about timing. A common question from founders is whether they can "beat" the upcoming tax changes.

Business Asset Disposal Relief (BADR), which reduces the Capital Gains Tax (CGT) rate on qualifying disposals, is currently 14% for gains realised before 6 April 2026. From that date, the rate rises to 18%. While a four-percentage-point increase is significant - representing £40,000 of additional tax for every £1 million of qualifying gain - it is essential to recognise that as of mid-March, the window to initiate and close a new deal before the April deadline has effectively closed.

A quality M&A transaction typically requires six to nine months of intensive work. Attempting to rush a deal in three weeks to save 4% in tax is a high-risk strategy that often leads to poor deal structures, price chips during due diligence, or total deal failure. Our advice is clear: do not let the tax tail wag the commercial dog. A well-prepared exit that achieves a 10% higher valuation through competitive tension far outweighs the 4% tax saving of a rushed, sub-optimal sale.

For those seeking long-term tax efficiency, the Employee Ownership Trust (EOT) remains a compelling alternative, despite the recent changes in November 2025. The EOT remains a powerful tool for founders who prioritise legacy, staff retention, and a smoother transition over the maximum upfront cash-out of a trade sale.

Deal Structures: Navigating the "Bridge"

Even in a buoyant 2026 market, buyers remain disciplined. We often describe current deal structures as "opportunistic but heavily guarded." This means that while headline valuations are high, the guaranteed cash at completion may be lower than in previous cycles.

Buyers are increasingly using three mechanisms to bridge valuation gaps:

- Earn-outs: Payments contingent on the business hitting specific profit targets over 12–24 months post-sale.

- Deferred consideration: A fixed portion of the price paid at a later date - effectively an interest-free loan from you to the buyer.

- Vendor rollover: Requiring you to retain 10–25% of your equity in the business, rolling it into the buyer's new ownership structure to ensure you remain motivated during the transition.

Founder Insight: Why 20% Might Be Worth More Than 80%

Don't automatically dismiss a request to "roll" equity. If you sell 80% of your business to a private equity firm with a buy-and-build strategy, your remaining 20% is now part of a much larger, more diversified group. When that PE firm exits in five years at a higher multiple, that "second bite" can often be worth as much - or more - than the initial 80% you sold. It's about backing the horse you built, but with someone else's fuel.

These structures shift risk from the buyer to you. To protect your interests, earn-outs must be based on metrics you can actually control - Gross Profit rather than Net Profit, which a buyer can manipulate through head office cost allocations. Any deferred payment should be secured via an escrow account or a robust parent company guarantee.

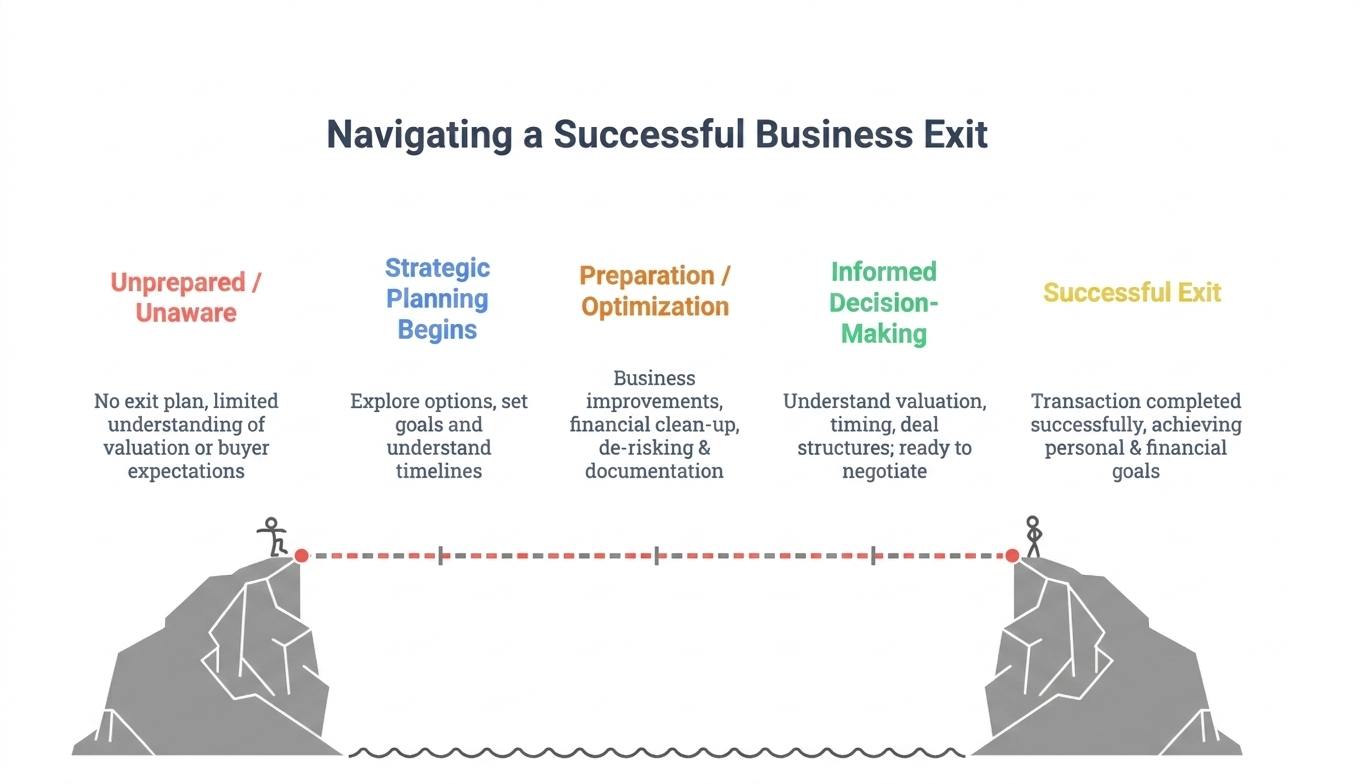

Positioning for a Premium Exit: The Manufacturing Checklist

Knowing the market is favourable is only half the battle. To command a premium, your business must be buyer-ready. In our experience supporting UK manufacturing exits, four areas consistently separate the best-in-class from the also-rans.

1. Financials Beyond Reproach

Buyers do not buy your statutory accounts; they buy your sustainable, normalised EBITDA. This is your profit adjusted for one-off costs, non-recurring income, and owner-related expenses that would not continue under new ownership. If you cannot evidence these adjustments with a clear audit trail, a buyer will simply ignore them - effectively devaluing your business.

Move beyond annual reporting to robust monthly management accounts that show a clear narrative of growth and margin stability. A manufacturing business with a strong, visible forward order book is far more attractive than one relying on historical figures alone.

2. Eradicating Owner Dependency

This is the single greatest value-killer in SME manufacturing. If the technical knowledge, key customer relationships, or emergency problem-solving all reside in your head, the business is a high-risk investment. To maximise value, you must make yourself redundant.

Founder Insight: The Ego vs. The Exit

The hardest part of exit planning isn't the spreadsheets; it's the psychology. As a founder, your identity is often woven into being the "fixer." However, in a sale process, every time a customer calls your mobile instead of the office, your valuation takes a hit. To a buyer, you are a single point of failure. True value is created when you can take a three-week holiday without checking your email - and the factory doesn't stop humming.

This involves formalising management structures, documenting proprietary processes through clear standard operating procedures, and empowering a leadership team that can run the factory floor and the sales office without your daily input. The irony of exit planning is that you need to make yourself dispensable to maximise what you are worth.

3. Pre-emptive Due Diligence

In 2026, due diligence is more forensic than ever. For manufacturers, this means a deep dive into environmental compliance, health and safety records, and the contractual landscape across your customer and supplier base.

🚩 Diligence Flag: The Invisible Veto

Review your top three customer contracts immediately for "Change of Control" clauses. Many specialist manufacturers are surprised to find that their biggest contracts can be terminated if the company is sold without the customer's prior written consent. If your most significant client doesn't approve of your buyer, they can walk away - and your deal value will evaporate overnight. Address these consents early in the process, not in the final week of diligence.

Identifying and resolving these issues 12 months before a sale is value creation. Finding them during a live deal is value destruction. Proactive preparation doesn't just speed up the process - it builds buyer confidence, and buyer confidence translates directly into better terms.

4. Assemble Your Advisory Team Early

A successful exit is not a DIY project. You require a coordinated team: a corporate finance or exit adviser to create competitive tension among buyers, an M&A solicitor who understands the nuances of manufacturing warranties, a tax specialist to navigate the 2026 complexities, and a wealth manager to plan your post-exit life. Engage this team 12 to 18 months before you plan to go to market. The preparation phase is where the real value is created.

The Window is Open: Your Next Steps

The fundamentals for specialist manufacturing exits in 2026 are exceptionally strong. The combination of strategic demand for UK capability and a massive surplus of investment capital has created a seller's market for high-quality assets. However, this window is defined by preparation, not just timing.

The businesses that achieve life-changing outcomes are not always the most profitable; they are the best prepared. They have clean financials, a management team that can operate independently, and a clear buyer-ready narrative that tells a compelling story to the right buyers.

If you are a specialist manufacturer considering your next chapter, the time to act is now - not next quarter, not next year. The preparation you undertake today directly determines the value you will realise when you eventually shake hands on a deal.

At Exit Strategy and Solutions, we work confidentially with manufacturing business owners to assess readiness, identify value drivers, and plan exits that deliver the outcomes you have worked so hard to earn. Get in touch for a no-obligation, confidential conversation about your business.

---------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

About Exit Strategy & Solutions

Exit Strategy & Solutions is a specialist advisory firm helping UK SME owners (typically £1-30M revenue) maximise business value and achieve successful exits. We provide strategic exit planning, readiness assessment, business valuation, founder decision support, and transaction support across all sectors.

Our approach combines deep market intelligence, strategic positioning expertise, and practical transaction experience to help owners achieve premium valuations and successful outcomes.

Ready to explore your exit options?

Take our Exit Readiness Calculator at www.exitstrategyandsolutions.com/exit-readiness-calculator to assess your business's exit readiness and identify opportunities to maximise value.

Contact us:

Email: enquiry@exitstrategyandsolutions.com

Phone: 0330 043 4689

Website: www.exitstrategyandsolutions.com

Disclaimer

This article is provided for informational purposes only and does not constitute financial, legal, tax, or investment advice. Every business situation is unique, and owners should consult with qualified professional advisors before making exit planning or transaction decisions.

Examples cited are based on composite scenarios created for illustrative purposes. Actual transaction terms, valuations, and outcomes vary based on specific circumstances.

Exit Strategy & Solutions is not responsible for decisions made based on information in this article. Professional advice tailored to your specific situation is essential for successful exit planning and execution.

Copyright © Exit Strategy & Solutions 2026. All rights reserved.